Research Commentary

AI/Tech Bubble Buildup: Bubbles Can Be Value Destructive During the Creation of New Industries

Global AI investment hit $252B and tech capex is set to reach 7.2% of GDP. Why this cycle's risk surfaces in debt markets — and why infrastructure owners emerge as the durable winners.

- $252.4BGlobal corporate AI investment, 2024

- 7.2%Projected tech capex as % of U.S. GDP, 2026

- 13×AI investment vs. 2014 levels

The headline statistics are hard to ignore. In 2024, global corporate AI investment reached $252.4 billion — a 25.5% increase from 2023, and now 13× higher than 2014 levels — which has provided the foundation for concerns around bubble formation.

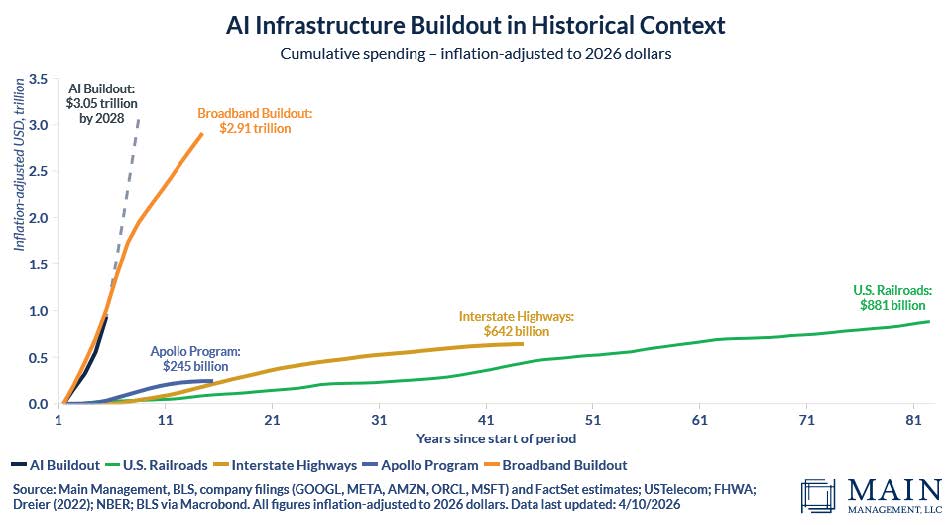

During the dot-com bubble, when the internet was first emerging, capital was allocated irrationally to unprofitable companies through speculative equity. At that bubble’s peak, tech capital expenditure on fiber-optic cables and network equipment reached 6.4% of U.S. GDP. Today, with current levels of pledged investment, tech capex is projected to reach 7.2% of GDP in 2026.

Fewer models, more infrastructure — the investment narrative has been rewritten

This surge in capital expenditure signals that the AI market is undergoing a fundamental shift in its competitive architecture, moving away from reliance on general-purpose model innovation toward dependence on electricity, advanced chips, and data-center infrastructure. Increased physical capacity and fewer models is the theme of the changing investment narrative.

Big Tech is rapidly ramping up capital expenditures, with spending projected to surge through 2026. Rather than competing on individual AI models, the broader strategy is to invest heavily in the infrastructure — data centers, compute, and cloud capacity — that powers the entire AI ecosystem. This reflects an industry-wide shift toward owning the foundational layers all AI development depends on, mirroring the dot-com era, where heavy investment in fiber-optic infrastructure accelerated capex and ultimately contributed to the bubble’s formation.

The financing threat: an excess of long-term debt

As capex accelerates through 2026, companies are financing these investments with a large amount of long-term debt, creating pressure as overall duration exposure in the debt market increases. While the dot-com bubble saw similar levels of investment, the key difference today is how it is financed. Instead of speculative equity, companies are relying more on long-term debt — and many AI firms are supported by real revenues, giving their business models a level of fundamental stability in contrast with the dot-com era, where valuations were driven more by expectations and speculation than actual performance.

As a result, debt markets are entering a period of elevated scrutiny, where the supply of long-term debt is no longer easily accommodated. Debt markets are positioned as the primary channel where value destruction will materialize as the bubble deflates — a natural and anticipated feature of such cycles rather than a cause for alarm.

What’s different this time?

Dot-com era

- Speculative equity funded unproven business models

- Value destruction hit equity markets first

- Infrastructure had no revenue foundation to survive the collapse

Today's AI cycle

- Long-term debt finances companies with real revenues

- Stress surfaces in debt markets, not equity

- A select group of infrastructure owners will emerge as durable winners

Who will prevail? Infrastructure ownership today is market leadership tomorrow

When the AI bubble deflates, the winners will not be those who led in model development, but those who established early control over the underlying infrastructure. By building and controlling essential infrastructure and energy supply, these firms create durable, revenue-generating assets that let them capture value regardless of which AI applications ultimately succeed. This dynamic mirrors the railroads, where long-term value accrued not to those speculating on routes, but to those who secured and scaled the physical networks themselves.

The question is not whether to participate in AI — it is how

Structurally, the answer is yes: AI exposure belongs in most well-constructed portfolios. But how you participate matters enormously. The distinction between durable infrastructure beneficiaries and speculative names that will not survive the eventual correction is best made at the model level — with research-driven sector and thematic positioning rather than concentrated single-name bets that go in and out of favor with the news cycle.

For advisors, the opportunity is not reacting to the bubble debate in real time — it is positioning portfolios with a disciplined framework that captures the structural buildout while managing the drawdown risk that historically accompanies cycles of this scale. This kind of work is at the core of how we partner with advisors through our Custom Model Partnerships, co-creating model portfolios that align preferred managers and asset-class views with our institutional, research-driven, risk-aware framework.

- 01LearnWe start by fully understanding your business and clients.

- 02BuildWe co-create custom model portfolios through an iterative partnership.

- 03ImplementThe best model is the one you're comfortable with.

- 04PartnerOngoing reviews, market commentary, and practice-management support.

All metrics from Morningstar Direct, Macrobond, and FactSet Financial Data and Analytics. This material is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. It reflects the opinion of Main Management as of the date written and is subject to change. All investing involves risk, including the possible loss of principal. Past performance does not guarantee future results.