Introduction

The unprecedented negative performance in both bonds and equities in 2022 has led investors and financial advisors to seek alternative investment strategies to diversify their portfolios and manage risk more effectively. Hedged equity strategies have garnered increasing popularity within the broader alternatives space in recent years, primarily due to their ability to function as resilient, all-weather investments during volatile and uncertain periods.

When properly implemented, hedged equity strategies may offer potential additional income and reduced volatility. We believe that a 5-15% permanent allocation to hedged equity strategies—funded from a blend of equity and fixed income—can provide an attractive complement to a well-diversified portfolio, enhancing its overall risk-return profile. A CBOE Global Markets 2017 study found that options-based funds experienced lower volatility and better risk-adjusted returns compared to traditional stock and commodity indexes, highlighting the protective role and performance optimization potential of hedged equity strategies in a portfolio. ₁ In this context, identifying the right hedged equity strategy is essential to navigate the market landscape and address the various risks and opportunities that financial advisors may encounter. With a GIPS-verified Composite, the BuyWrite strategy has been actively managed for nearly 20 years. Accordingly, our team at Main Management has been at the forefront of the ETF hedged equity universe. This report aims to provide guidance on analyzing hedged equity strategies and key factors to consider, such as choosing the right hedging method, active vs. passive management, sustainable yield, tax efficiency, and transparency and risk management.

When properly implemented, hedged equity strategies may offer potential additional income and reduced volatility. We believe that a 5-15% permanent allocation to hedged equity strategies—funded from a blend of equity and fixed income—can provide an attractive complement to a well-diversified portfolio, enhancing its overall risk-return profile. A CBOE Global Markets 2017 study found that options-based funds experienced lower volatility and better risk-adjusted returns compared to traditional stock and commodity indexes, highlighting the protective role and performance optimization potential of hedged equity strategies in a portfolio. ₁ In this context, identifying the right hedged equity strategy is essential to navigate the market landscape and address the various risks and opportunities that financial advisors may encounter. With a GIPS-verified Composite, the BuyWrite strategy has been actively managed for nearly 20 years. Accordingly, our team at Main Management has been at the forefront of the ETF hedged equity universe. This report aims to provide guidance on analyzing hedged equity strategies and key factors to consider, such as choosing the right hedging method, active vs. passive management, sustainable yield, tax efficiency, and transparency and risk management.

Section 1: Choosing the Right Hedging Strategy

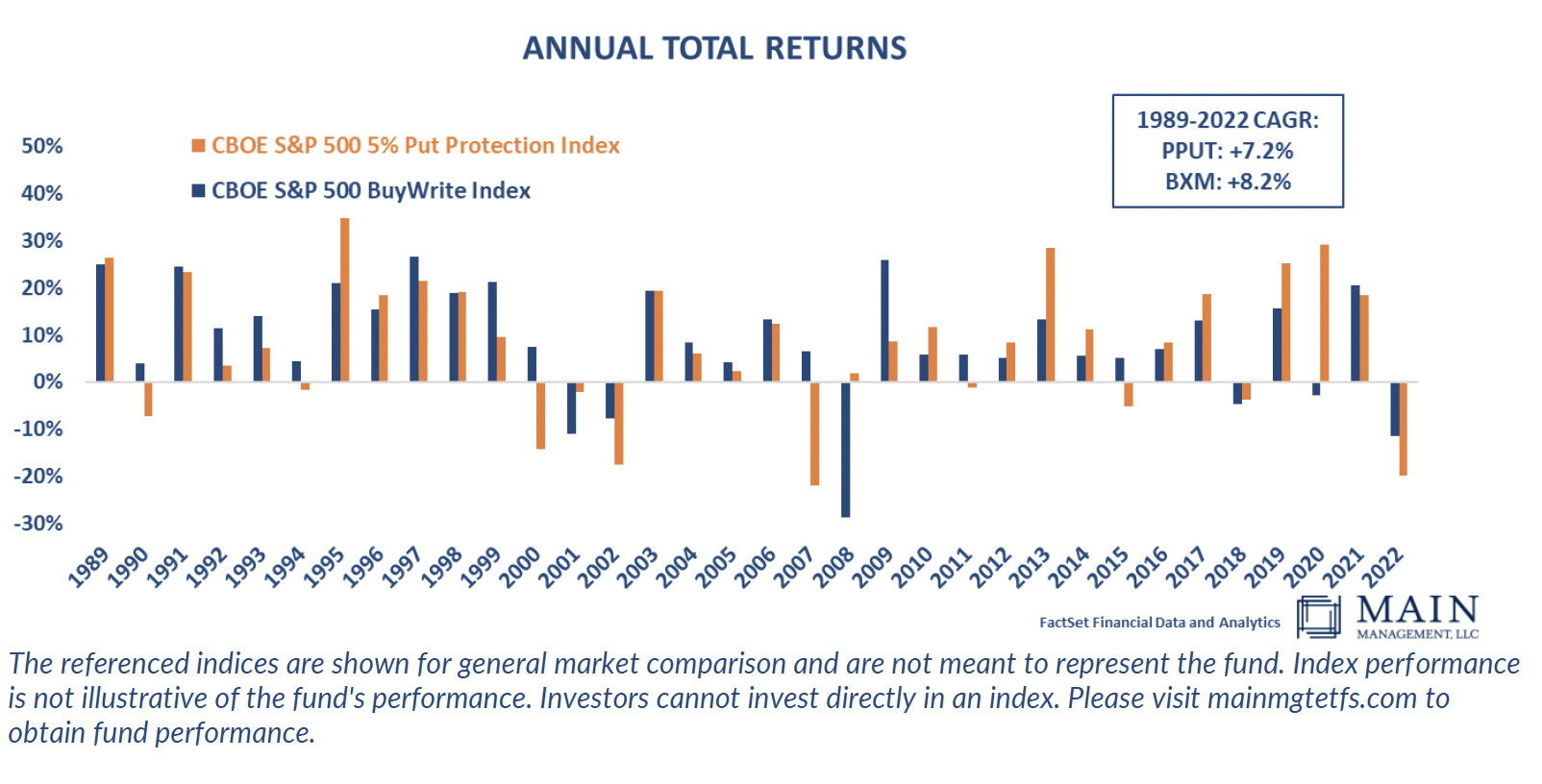

Selecting a strategy with the appropriate hedging method, either buying puts or selling calls, may significantly impact the performance and risk profile of a hedged equity strategy. Both approaches have their advantages and drawbacks: buying puts may offer downside protection but requires precise market timing and can incur higher costs, while selling (writing) calls may generate consistent income to offset potential losses but may cap upside potential. In the Main BuyWrite strategy, we employ call-writing because we believe it offers a more consistent income stream and aligns with our expertise and enables us to work on both parts of the portfolio synergistically. Financial advisors should understand the hedging method used by the strategy and how it fits within their clients’ risk tolerance and investment objectives.

1. “Performance Analysis of Option-Based Equity Mutual Funds, CEFs, and ETFs: An Update” (January 2018)

1. “Performance Analysis of Option-Based Equity Mutual Funds, CEFs, and ETFs: An Update” (January 2018) - https://cdn.cboe.com/resources/education/research_publications/performance-options-based-funds.pdf

The chart above compares the performance of the CBOE S&P 500 BuyWrite Index (BXM), which employs a covered call writing strategy, with the CBOE S&P 500 5% Put Protection Index (PPUT), which utilizes put buying as a hedge. The historical returns highlight the advantages of the covered call approach, especially during protracted down markets, such as the one witnessed in 2022. This chart also illustrates the importance of selecting a hedging strategy that aligns with market conditions and clients’ investment goals.

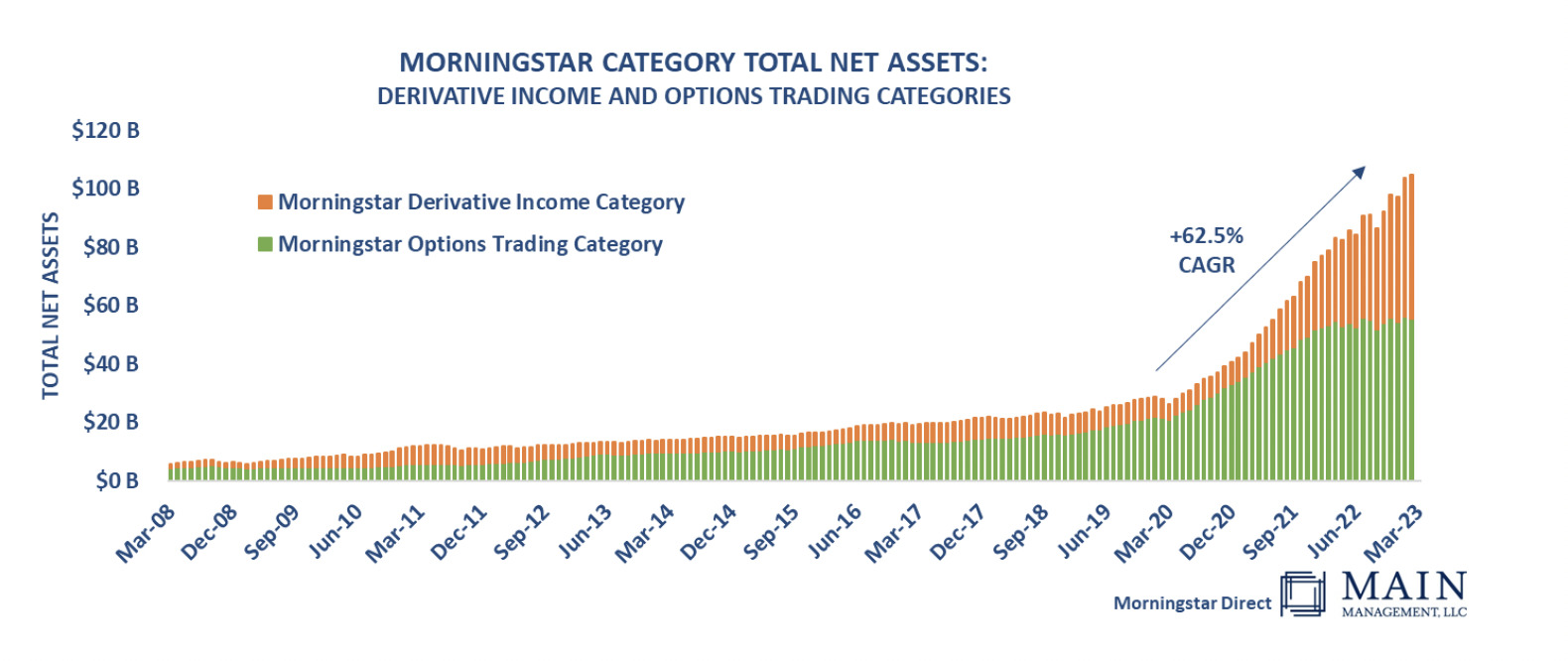

Section 2: Active vs. Passive Management

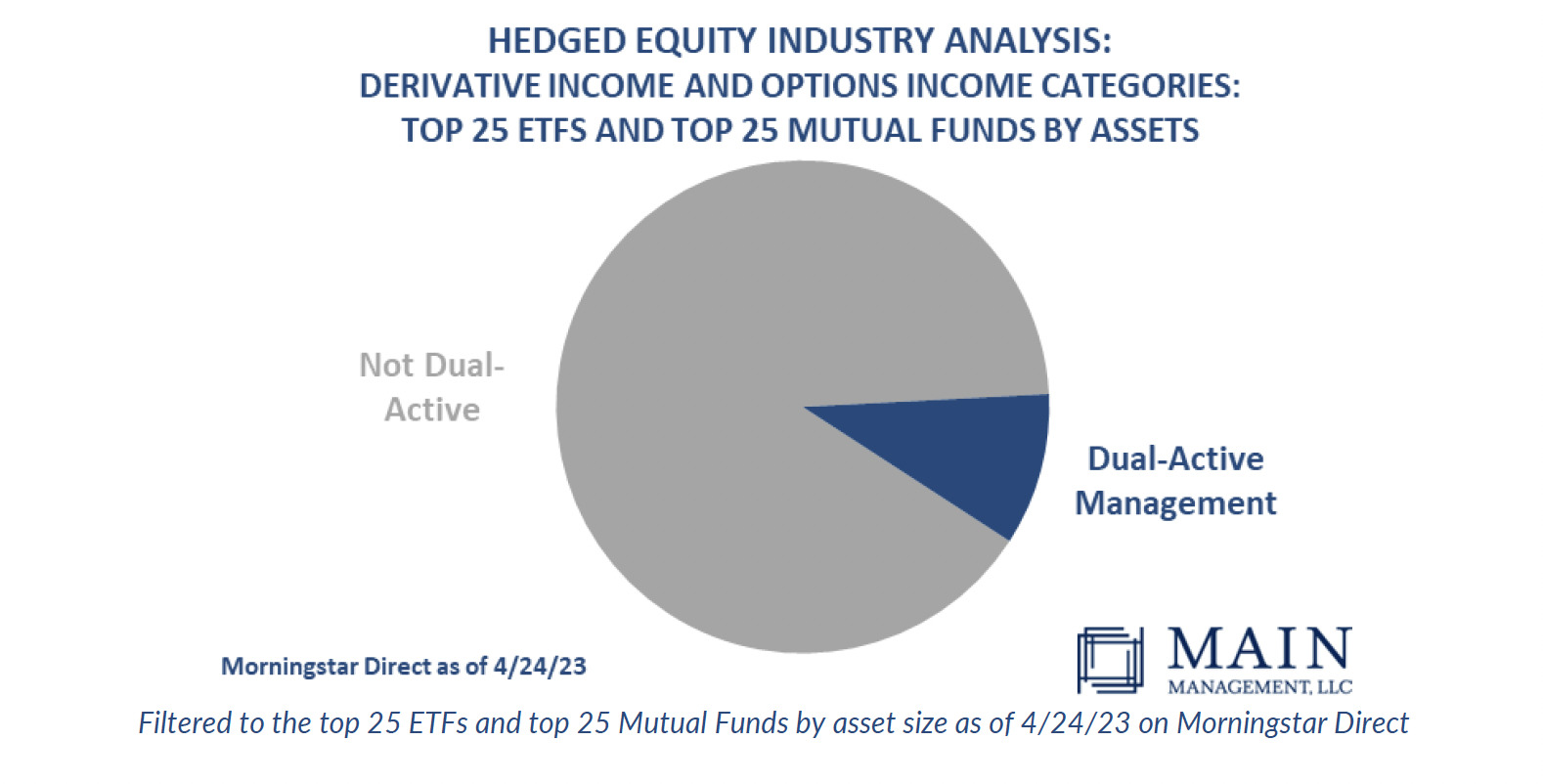

Investors must also consider the trade-offs between active and passive management in both the equity allocation and options trading within the strategy, as the methodology may significantly impact a strategy’s performance. Typically, strategies choose to be active in either the equity allocation or options trading, or even completely passive in both. We believe that active management is a critical component in a hedged equity strategy, particularly because of the many varied considerations within the strategy.

Among a sample of the top 25 ETFs and top 25 mutual funds in the Morningstar Derivative Income and Options Trading categories, we identified merely five that boast an investment process that actively manages both the equities and the options overlay. In contrast, the remaining strategies either passively track an index on the equity side and/or adopt a completely systematic approach on the options side. The Main BuyWrite distinguishes itself with a harmonious, dual-active methodology encompassing both equity allocation and options hedging that has been running for nearly 20 years. This approach allows us to seize market opportunities and adeptly manage risk by concurrently evaluating the underlying equities and the options overlay.

Section 3: Sustainable Yield vs. Self-Liquidating Funds

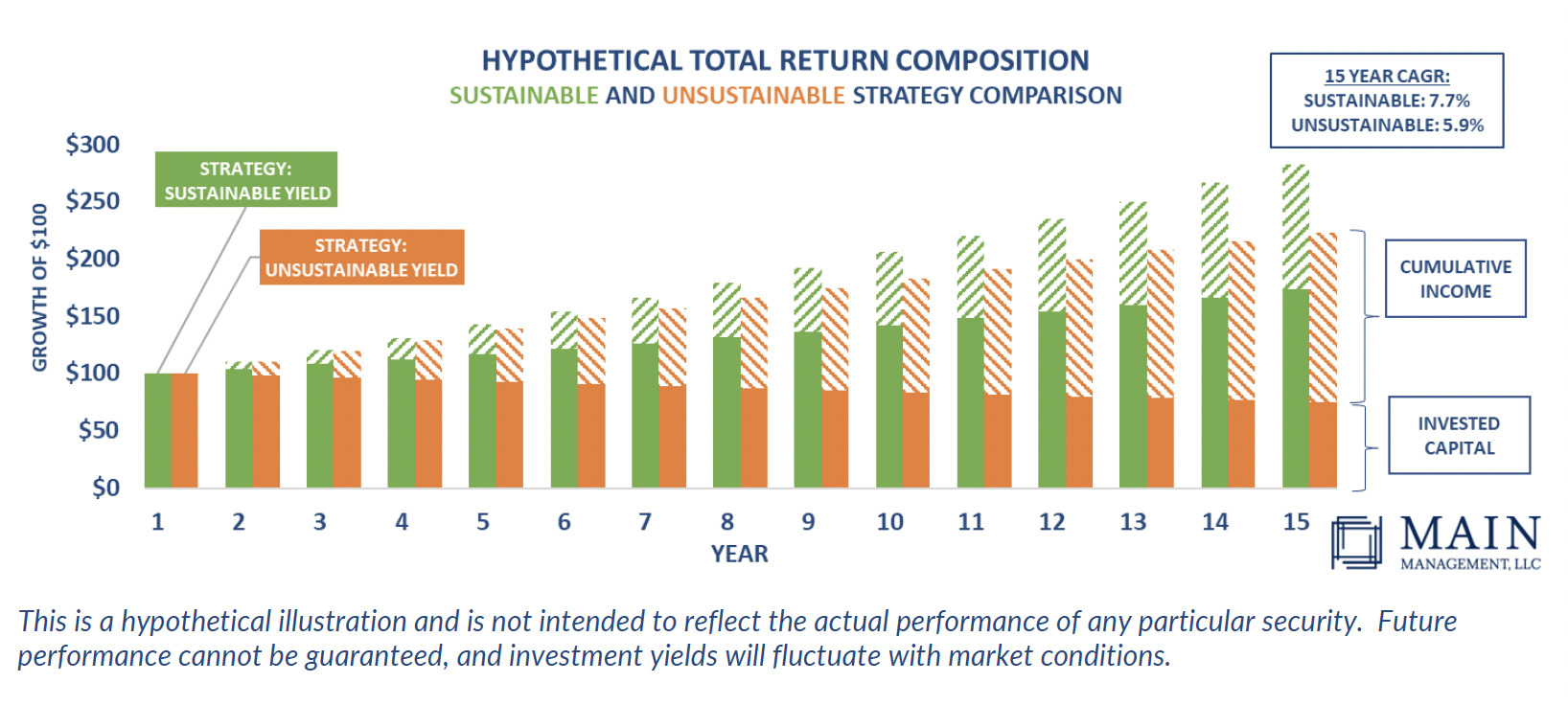

While high yields can be attractive, excessively high yields may potentially lead to strategies that are essentially “self-liquidating.” Often, these strategies may give up potential capital growth for unsustainably high income, leading to declining or stagnant capital over time. In other words, if the yield on a strategy seems too good to be true, that may well be the case. Financial advisors may want to prioritize strategies that balance income generation and capital growth for long-term value.

This is a hypothetical illustration and is not intended to reflect the actual performance of any particular security. Future performance cannot be guaranteed, and investment yields will fluctuate with market conditions.

The chart above is not a projection of the Main BuyWrite strategy’s performance or any security in particular. Rather, the above purely serves as a visual comparison between the returns of two hypothetical, identical strategies with a 10% annual return on invested capital, with the only distinction being the annual yield: the “sustainable strategy” pays a 6% annual yield, while the “unsustainable strategy” offers a 12% annual yield. Each strategy’s total return per year consists of two components: the growth of the invested capital and the cumulative income generated from the yield over time.

Initially, the unsustainable yield strategy (12%) seems to perform on par with the lower-yielding strategy (6%) during the first few years. However, as time progresses, the disparity in total returns starts to widen. In fact, the unsustainable strategy experiences a decline in invested capital each year, essentially sacrificing capital growth for income. This growing divergence can be attributed to the power of compounding, where choosing higher distributions hinders returns from compounding upon themselves.

While some investors may be content with negligible or even negative capital growth in exchange for higher income, it’s vital to recognize that unsustainable yield strategies cannot “have their cake and eat it too.” Opting for a strategy with unsustainably high yields may increase the likelihood of forfeiting potential capital growth, which could lead to long-term repercussions. Our Main BuyWrite aims to achieve a sustainable yield that strikes a balance between income generation and capital growth, intending to deliver continued value to investors while fulfilling their income objectives.

Section 4: Tax Efficiency

Income generation is not a one-size-fits-all approach, as various tax implications and considerations can arise depending on the management of a hedged equity strategy. We believe that financial advisors may want to prioritize strategies that demonstrate tax-awareness to ensure optimal outcomes for their clients. The Main BuyWrite exemplifies this focus on tax efficiency through its active management of both the equity allocation and options writing components, consistently monitoring tax implications. By contrast, many other hedged equity strategies, particularly passive ones, may inadvertently accumulate significant tax liabilities due to the income they distribute.

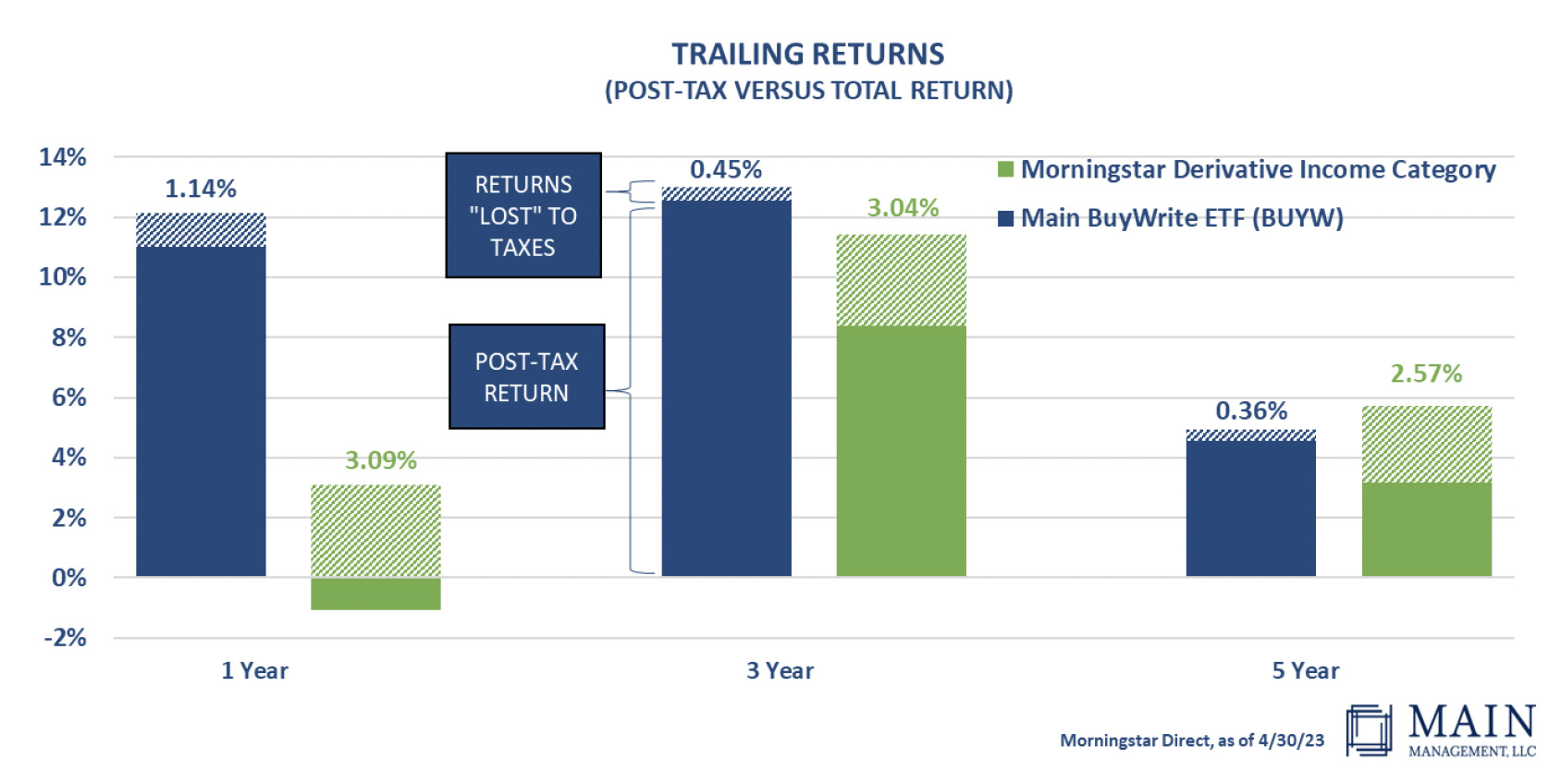

This stacked bar chart illustrates the tax efficiency of various hedged equity strategies, as measured by the difference between the pre-tax and post-tax annualized returns over the trailing 3 years, according to Morningstar Direct. The Main BuyWrite ETF (BUYW) demonstrates a higher level of tax-awareness, with considerably less of its returns lost to taxes compared to the those in the Morningstar Derivative Income Category and Options Trading Category. This comparison highlights the importance of tax efficiency and showcases the benefits of the Main BuyWrite ETF’s active management and tax-aware approach.

Section 5: Transparency and Risk Management

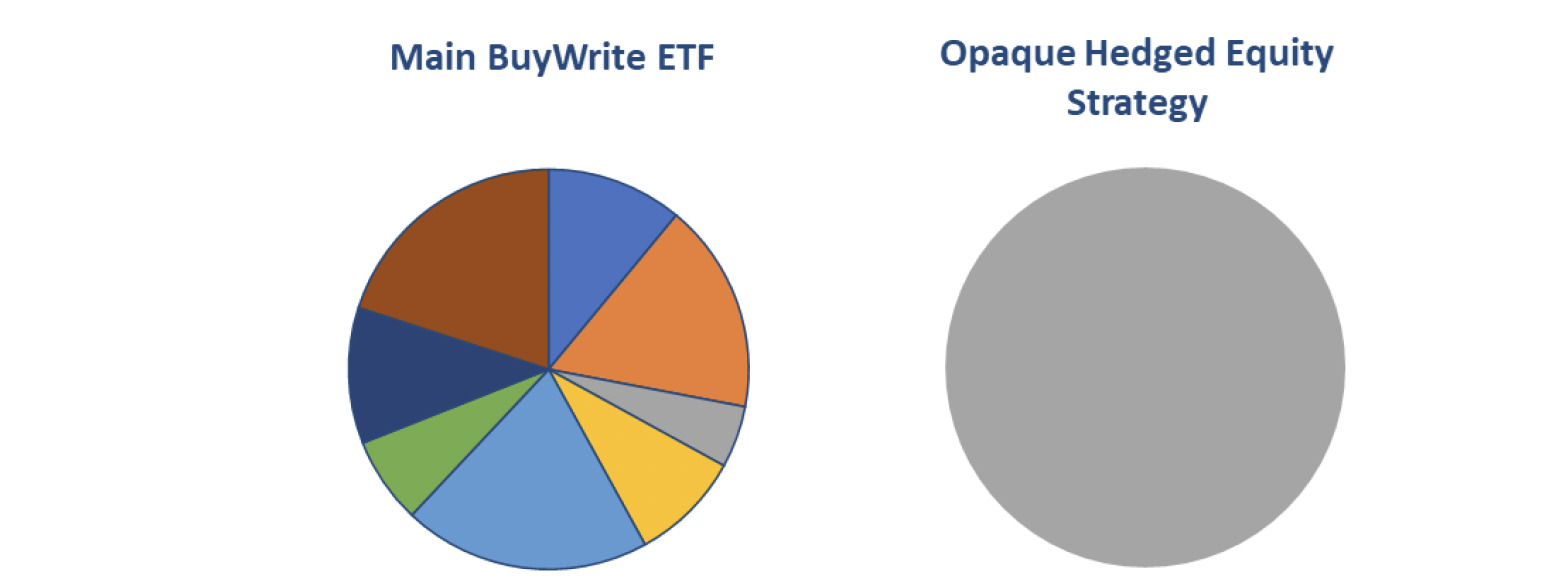

Transparency and risk management are essential components of any investment strategy, as they enable financial advisors to make more informed decisions on behalf of their clients. Some hedged equity strategies can be opaque or overly complex, making it difficult for investors to understand the underlying holdings and associated risks. The Main BuyWrite ETF prides itself on its transparency, with clear daily disclosure of holdings and no use of complex derivatives like OTC equity swaps. 2 Moreover, the strategy’s simplicity, focusing on equity selection and covered calls written as an overlay, allows for a more straightforward approach. Our management is a key differentiator – and not opaque derivatives – as we navigate the nuanced decisions on both parts of the portfolio. This transparency and simplicity enables investors and financial advisors to better assess the risks and potential rewards of the strategy, making informed decisions for their clients.

Conclusion

Incorporating a hedged equity strategy in client portfolios may offer financial advisors a unique value proposition, providing something different and additive outside the generic equity/fixed income portfolio. This approach may help strengthen client relationships while helping dampen portfolios against market volatility, although this may entail limiting the strategy’s upside. By considering factors such as hedging methods, active vs. passive management, sustainable yield, tax efficiency, and transparency and risk management, financial advisors may make informed decisions when allocating hedged equity strategies to their clients’ portfolios. We encourage financial advisors to explore the Main BuyWrite strategy and consider its potential benefits for their clients’ portfolios, as it offers a unique combination of experience, active management, and a focus on long-term value.

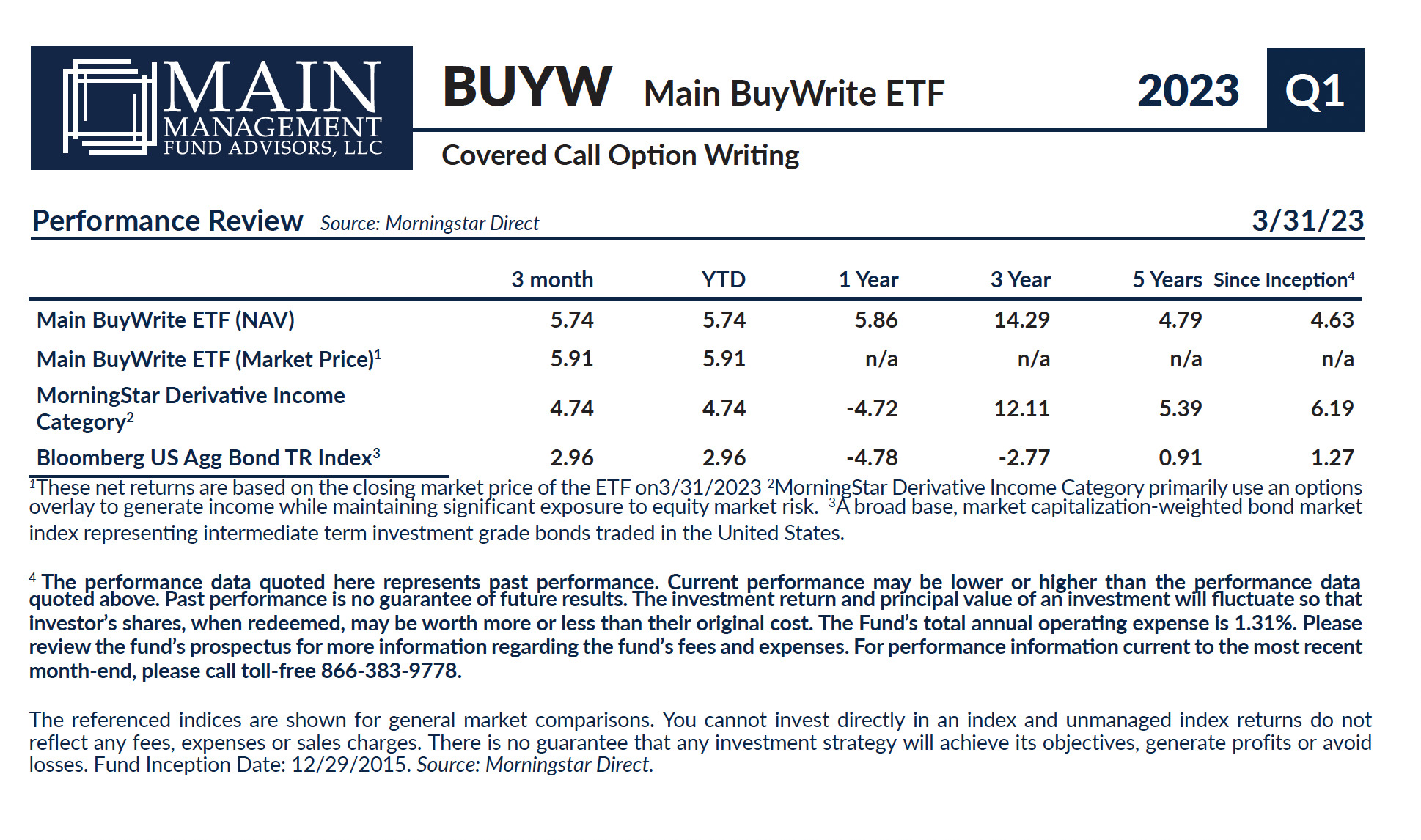

BUYW Main BuyWrite ETF Covered Call Option Writing

BUYW Main BuyWrite ETF Covered Call Option Writing

Source: Morningstar Direct

Performance Review 3/31/23

Investors should carefully consider the investment objectives, risks, charges and expenses of the Main BuyWrite Fund. This and other important information about the Fund is contained in the prospectus, which can be obtained by calling 1-866-383-9778. The prospectus should be read carefully before investing. The Main BuyWrite Fund is distributed by Northern Lights Distributors, LLC, Member FINRA/SIPC. Main Management Fund Advisors, LLC is not affiliated with Northern Lights Distributors, LLC.

FUND’S RISK DISCLOSURES

There is the risk that you could lose money through your investment in the Fund. The Fund may have significant exposure to a limited number of issuers conducting business in the same sector or group of sectors. Market conditions, interest rates, and economic, regulatory, or financial developments could significantly affect a single sector or a group of sectors. ETF’s are subject to specific risks, depending on the nature of the underlying strategy of the fund. These risks could include liquidity risk, sector risk, as well as risks associated with fixed income securities, real estate investments, and commodities, to name a few. As a seller (writer) of a put option, the Fund will tend to lose money if the value of the reference index or security falls below the strike price. As the seller (writer) of a call option, the Fund may experience lower returns if the value of the reference index or security rises above the strike price. Investments in foreign securities could subject the Fund to greater risks including, currency fluctuation, economic conditions, and different governmental and accounting standards. The earnings and prospects of small and medium sized companies are more volatile than larger companies and may experience higher failure rates than larger companies. Options DisclosureThe options in which the Fund invests are derivatives. They involve risks different from, and in some respects greater than, the risks associated with investing in more traditional investments, such as stocks and bonds. Derivatives can be highly complex and highly volatile and may perform in unanticipated ways. Derivatives can be difficult to value and may at times be highly illiquid. Derivatives may create leverage, and the loss on derivative transactions may substantially exceed the Fund’s initial investment. Some derivatives have the potential for unlimited losses.*Distributions in excess of the Fund’s current and accumulated earnings and profits are treated as a tax-free return of capital to the extent of your basis in Shares and as capital gain thereafter. A distribution will reduce the Fund’s NAV per Share and may be taxable to you as ordinary income or capital gain (as described above) even though, from an investment standpoint, the distribution may constitute a return of capital.

Main Management, LLC (“Main Management”, or the “Firm”) is an investment adviser registered under the Investment Advisers Act of 1940, as amended. The Firm was founded in 2002 and provides investment management services primarily to high net worth, family groups, foundations/endowments, and serves as a sub-adviser to third-party investment advisers & broker-dealers. The information contained herein was prepared using sources that the Firm believes are reliable, but the Firm does not guarantee its accuracy. The information reflects subjective judgments, assumptions and the Firm’s opinion on the date made and may change without notice. The Firm is not obligated to update this information. Nothing herein should be construed as investment advice or a recommendation to purchase or sell securities. The information is not intended as an offer to provide advisory services in any state or jurisdiction where such offer would not be permitted under applicable registration requirements. All equity investing entails risk of loss. In preparing this material, Main Management has not taken into account the investment objectives, financial situation or particular needs of any individual investor. Many securities transactions are risky and are not suitable for all investors. All securities investments carry risk, including a risk of loss of principal.

1595-NLD-05112023